In today’s newsletter, Dumpling Bullish, independent digital asset commentator, writes about the growing influence of bitcoin’s derivatives stack on its price.

Then, in Ask an Expert, Leo Mindyuk from ML Tech, answers questions about the evolution of bitcoin investment products.

– Sarah Morton

Bitcoin price discovery: no longer just a demand story

For most of its history, bitcoin had a simple pricing logic: limited supply, growing demand and the occasional panic in between. That logic still exists. It just no longer runs the show.

What runs the show now is the derivatives stack sitting atop the asset.

From spot market to leverage system

Over the past decade, bitcoin has moved from a predominantly spot-driven market into a layered derivatives ecosystem. Futures, perpetual swaps, options, exchange-traded funds (ETFs), structured products and prime brokerage lending have transformed the way price discovery occurs.

CME futures launched in December 2017, giving institutions a regulated, scalable way to short bitcoin for the first time and providing a mechanism to express bearish views at the top of what had been a 19x run. The asset saw an 80% drawdown. That did not kill bitcoin. It allowed disagreement to be priced more efficiently.

Then came the 2024 ETF approvals, acting as the foundation for a new derivatives layer inside U.S. equity markets.

Each addition didn't change what bitcoin is. It changed where and how its price gets discovered.

Three variables that now matter most

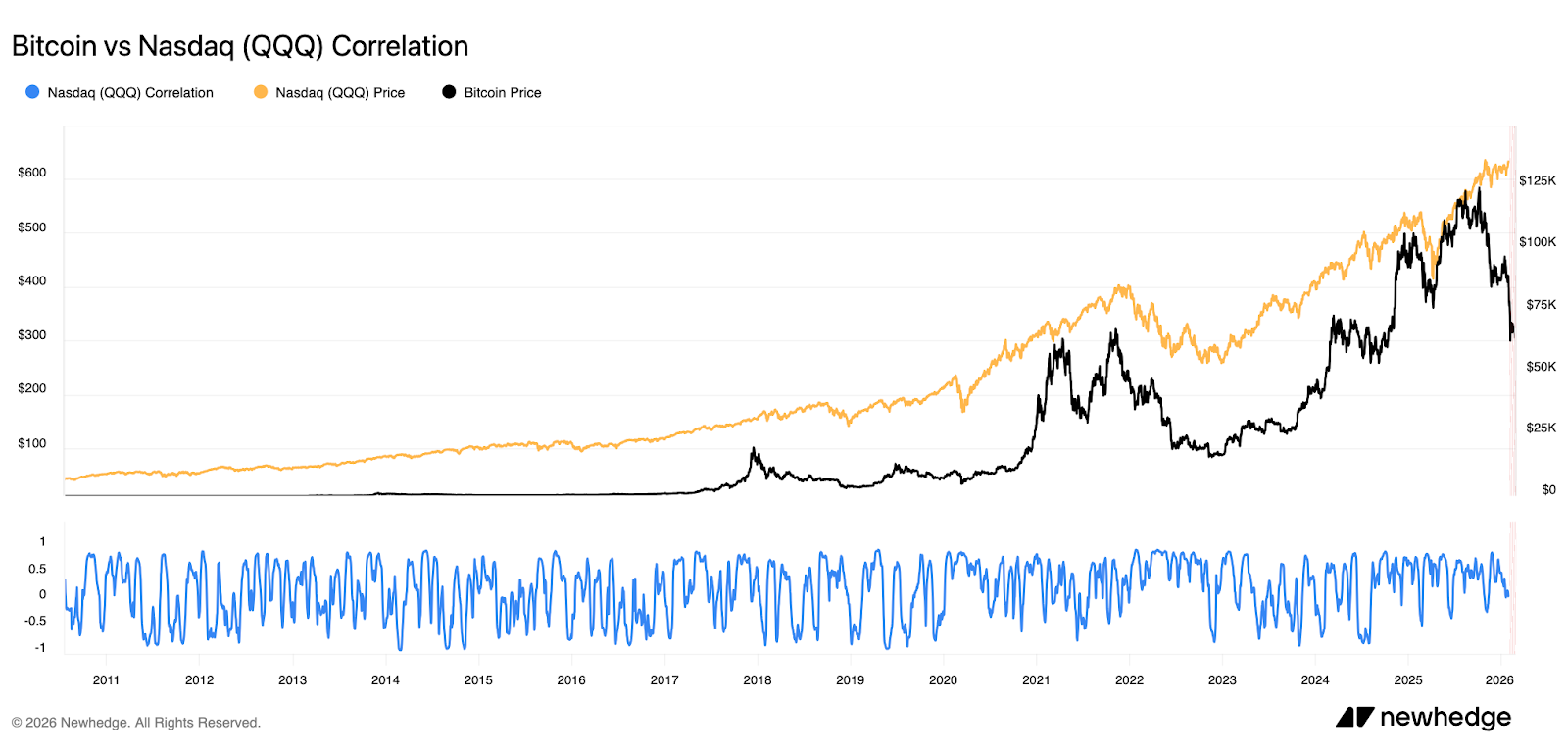

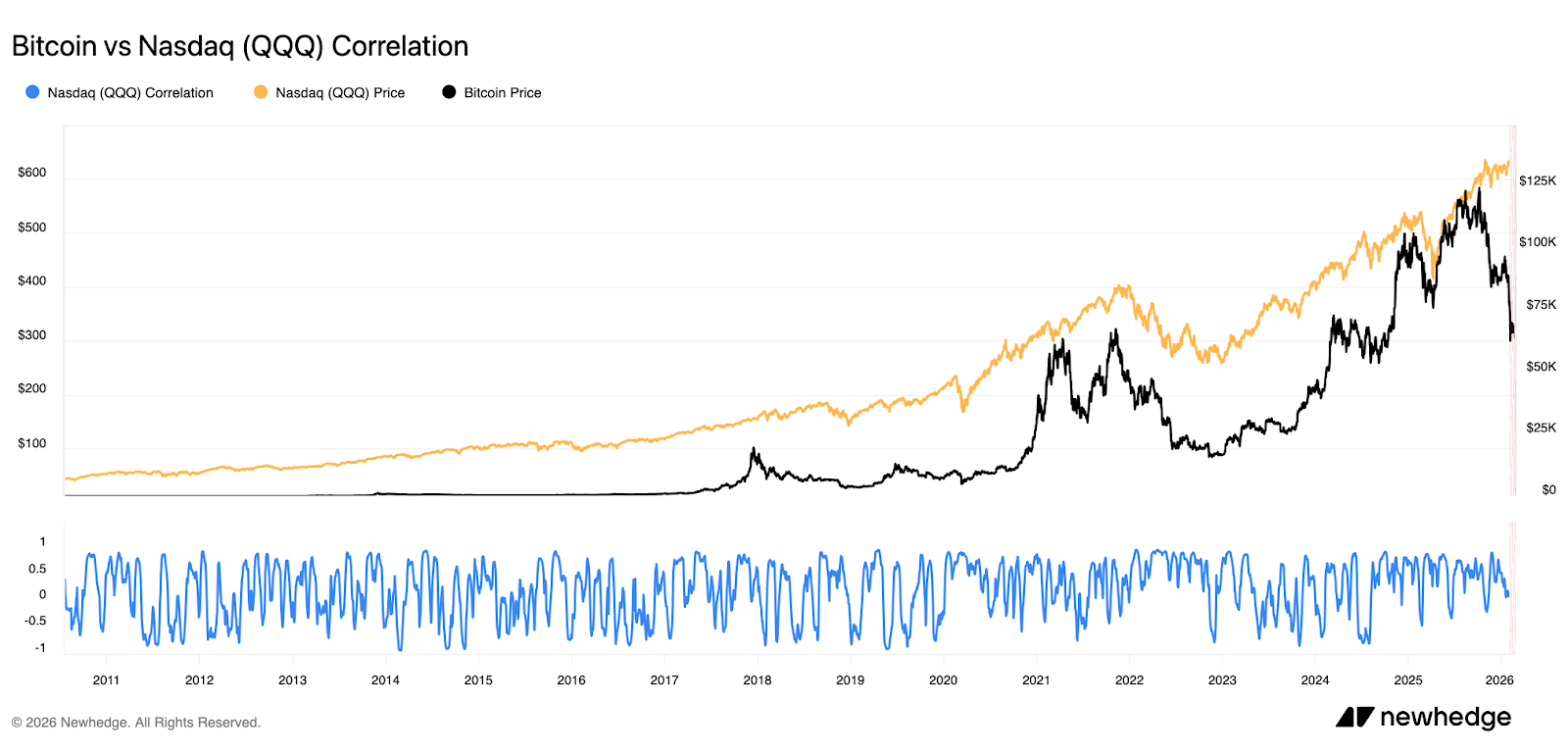

Real yields and dollar strength set the macro backdrop. Bitcoin has increasingly traded as a high-beta liquidity asset and when global risk appetite contracts, it sells off alongside equities and other risk assets, regardless of what the blockchain is doing.

Bitcoin 30-day rolling correlation with Nasdaq (QQQ), 2011 – present

Source: Newhedge

Derivatives positioning tells the short-term story. CME open interest and perpetual funding rates reveal whether a price move is built on genuine new demand or on leveraged speculation that will eventually unwind violently. When funding rates run persistently positive, the market is paying a premium to be long — and that premium is a fragility signal.

Bitcoin CME futures open interest and price, Dec 2017 – present

Source: CME Group via TradingView

ETF options mechanics have introduced a new transmission channel. When institutional investors buy calls or puts on the iShares Bitcoin Trust ETF (IBIT), dealers who sell those options must hedge by trading the underlying ETF and, in some cases, related futures or spot exposure. This hedging is procyclical. When Bitcoin rises, dealers must buy more; when it falls, they must sell. Modest directional moves get mechanically amplified. The result is that a meaningful share of Bitcoin's short-term volatility is now generated mainly by equity market structure.

Financialization is not extinction

Gold offers a useful parallel. The development of futures and ETFs did not eliminate gold’s scarcity. It integrated gold into global macro portfolios and amplified its volatility during liquidity cycles. Bitcoin is undergoing a similar integration process at a faster pace. It is being absorbed into the global risk budget system. That absorption brings institutional capital, liquidity, and legitimacy. It also brings correlation, reflexivity, and the occasional violent unwind driven by forces that have nothing to do with the protocol.

Scarcity remains intact at the protocol level. But its influence on price is increasingly subordinated to the cost of capital and the mechanics of the derivative stack. Bitcoin is not losing its scarcity narrative. It is gaining a liquidity identity.

Scarcity anchors the asset. Liquidity sets the marginal price.

– Dumpling Bullish, independent digital asset commentator

Ask an Expert

Q: Over the past few years, bitcoin investment products have expanded from spot exposure to futures, options and ETFs. How do you see the evolution of bitcoin financial products shaping the way investors access the asset?

The evolution of bitcoin investment products mirrors the path we’ve seen in traditional asset classes. Early participants primarily accessed bitcoin through direct ownership — buying and holding the asset itself on crypto exchanges. Over time, as institutional interest increased, the market began developing a broader toolkit: regulated futures and options, structured products and regulated fund structures and more recently, spot ETFs.

This expansion is important because it changes bitcoin from simply being a speculative asset to something that can be integrated into portfolio construction and risk management frameworks. Different investors have different needs. Some want direct exposure to the asset’s price movement, while others want regulated vehicles, derivatives for hedging or ways to express more nuanced market views.

As the ecosystem matures, financial products make Bitcoin easier to access through familiar structures, which lowers barriers for institutional investors and broadens the ways the asset can be incorporated into diversified portfolios.

Q: In traditional markets, financial products often evolve from simple exposure to more complex structures like leveraged, inverse, and derivatives-based strategies. Are we starting to see a similar progression in the bitcoin ecosystem?

Yes, and it’s a natural progression. In most asset classes, markets begin with simple spot exposure and gradually develop layers of financial instruments that allow investors to manage risk, hedge positions or express different market views. Bitcoin is following that same trajectory.

Initially, the focus was simply on gaining exposure to the asset itself. Today, we’re seeing a more developed ecosystem that includes derivatives, volatility trading and structured products. These tools allow investors to do much more than just speculate on price appreciation. They can hedge downside risk, trade volatility or construct market-neutral strategies.

What’s interesting is that crypto markets often evolve faster than traditional markets because the infrastructure is digital and global. As liquidity deepens and regulatory frameworks become clearer, we’ll likely see even more sophisticated products emerge that resemble strategies commonly used in equities, commodities and fixed-income markets. For example, I expect growth in various income-generating ETFs — instruments for inversed, leveraged or broader crypto factor-based exposure. Moreover, we will likely see a tremendous growth in crypto option markets.

Q: With the growth of futures markets and the introduction of spot ETFs, how might the next generation of bitcoin products expand investor use cases, whether for hedging, leverage, or more sophisticated portfolio strategies?

Futures markets already allow investors to hedge exposure or express directional views without holding the asset directly. ETFs have made bitcoin accessible through traditional brokerage accounts. The logical next step is products that focus on portfolio outcomes.

As that happens, bitcoin starts to look less like a standalone trade and more like a portfolio building block. That’s ultimately where the market is heading: giving investors the flexibility to express views on the market in much more nuanced and sophisticated ways with the ease of access.

– Leo Mindyuk, CEO & CIO, ML Tech

Keep Reading

- Mastercard set to acquire stablecoin infrastructure company BVNK for up to $1.8 billion, setting the stage to expand its crypto payments network.

- Australia's Senate moves forward with crypto asset regulation frameworks.

- The U.S. Securities and Exchange Commission issues first-ever definitions for which crypto assets are securities.